Europe Aluminium Cans Market Trends, Share, Size, Revenue, Demand and Future Outlook

Europe Aluminium Cans Market Growth, Size, Trends Analysis- By Application- Regional Outlook, Competitive Strategies and Segment Forecast to 2033

| Published: Nov-2024 | Report ID: PACK2422 | Pages: 1 - 157 | Formats*: |

| Category : Packaging | |||

- Vinca introduces organic Sicilian wine in 187-milliliter wine cans in Ardagh in December 2023. All of the wine market's demands for single-serve formats are satisfied by AMP's Wine Can line in a contemporary and sustainable manner. Aluminum beverage cans that are safe, lightweight, and infinitely recyclable are ideal for point-of-sale refrigeration, in-store handling, and shipping.

| Report Metric | Details |

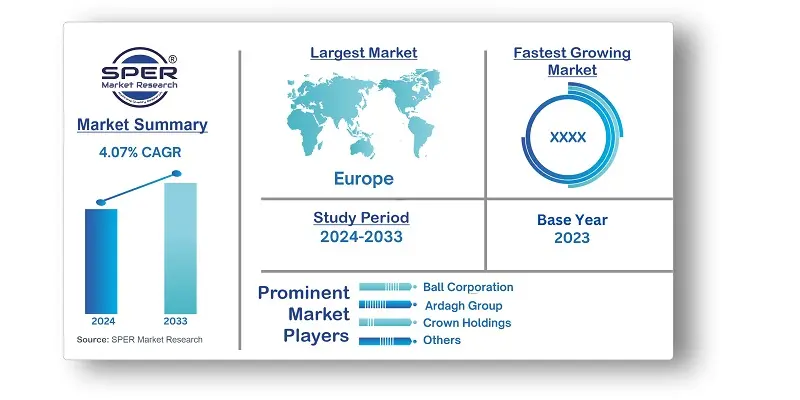

| Market size available for years | 2020-2033 |

| Base year considered | 2023 |

| Forecast period | 2024-2033 |

| Segments covered | By Application |

| Regions covered | France, Germany, Italy, Spain, United Kingdom, Rest of Europe. |

| Companies Covered | Ball Corporation, Ardagh Group, Crown Holdings, Inc., Silgan Holdings Inc., CAN-PACK SA, Massilly Holding SAS, Tecnocap Group, and Tata Europe Ltd. |

- Beverage Manufacturers

- Packaging Suppliers

- Retailers and Distributors

- Environmental and Sustainability Organizations

- End Consumers

- Regulatory Bodies

- Recycling Companies

| By Application: |

- Europe Aluminium Cans Market Size (FY’2024-FY’2033)

- Overview of Europe Aluminium Cans Market

- Segmentation of Europe Aluminium Cans Market By Application (Beverages, Food, Others)

- Expansion Analysis of Europe Aluminium Cans Market

- Problems and Obstacles in Europe Aluminium Cans Market

- Competitive Landscape in the Europe Aluminium Cans Market

- Impact of COVID-19 and Demonetization on Europe Aluminium Cans Market

- Details on Current Investment in Europe Aluminium Cans Market

- Competitive Analysis of Europe Aluminium Cans Market

- Prominent Players in the Europe Aluminium Cans Market

- SWOT Analysis of Europe Aluminium Cans Market

- Europe Aluminium Cans Market Future Outlook and Projections (FY’2024-FY’2033)

- Recommendations from Analyst

1.1. Scope of the report1.2. Market segment analysis

2.1. Research data source2.1.1. Secondary Data2.1.2. Primary Data2.1.3. SPER’s internal database2.1.4. Premium insight from KOL’s2.2. Market size estimation2.2.1. Top-down and Bottom-up approach2.3. Data triangulation

4.1. Driver, Restraint, Opportunity and Challenges analysis4.1.1. Drivers4.1.2. Restraints4.1.3. Opportunities4.1.4. Challenges4.2. COVID-19 Impacts of the Europe Aluminium Cans Market

5.1. SWOT Analysis5.1.1. Strengths5.1.2. Weaknesses5.1.3. Opportunities5.1.4. Threats5.2. PESTEL Analysis5.2.1. Political Landscape5.2.2. Economic Landscape5.2.3. Social Landscape5.2.4. Technological Landscape5.2.5. Environmental Landscape5.2.6. Legal Landscape5.3. PORTER’s Five Forces5.3.1. Bargaining power of suppliers5.3.2. Bargaining power of buyers5.3.3. Threat of Substitute5.3.4. Threat of new entrant5.3.5. Competitive rivalry5.4. Heat Map Analysis

6.1. Europe Aluminium Cans Market Manufacturing Base Distribution, Sales Area, Product Type6.2. Mergers & Acquisitions, Partnerships, Product Launch, and Collaboration in Europe Aluminium Cans Market

7.1. Europe Aluminium Cans Market Size, Share and Forecast, By Application, 2020-20267.2. Europe Aluminium Cans Market Size, Share and Forecast, By Application, 2027-20337.3. Beverages7.4. Food7.5. Others

8.1. Europe Aluminium Cans Market Size and Market Share

9.1. Europe Aluminium Cans Market Size and Market Share By Region (2020-2026)9.2. Europe Aluminium Cans Market Size and Market Share By Region (2027-2033)9.3. France9.4. Germany9.5. Italy9.6. Spain9.7. United Kingdom9.8. Rest of Europe

10.1. Ball Corporation10.1.1. Company details10.1.2. Financial outlook10.1.3. Product summary10.1.4. Recent developments10.2. Ardagh Group10.2.1. Company details10.2.2. Financial outlook10.2.3. Product summary10.2.4. Recent developments10.3. Crown Holdings, Inc.10.3.1. Company details10.3.2. Financial outlook10.3.3. Product summary10.3.4. Recent developments10.4. Silgan Holdings Inc.10.4.1. Company details10.4.2. Financial outlook10.4.3. Product summary10.4.4. Recent developments10.5. CAN-PACK SA10.5.1. Company details10.5.2. Financial outlook10.5.3. Product summary10.5.4. Recent developments10.6. Massilly Holding SAS10.6.1. Company details10.6.2. Financial outlook10.6.3. Product summary10.6.4. Recent developments10.7. Tecnocap Group10.7.1. Company details10.7.2. Financial outlook10.7.3. Product summary10.7.4. Recent developments10.8. Tata Europe Ltd10.8.1. Company details10.8.2. Financial outlook10.8.3. Product summary10.8.4. Recent developments10.9. Others

SPER Market Research’s methodology uses great emphasis on primary research to ensure that the market intelligence insights are up to date, reliable and accurate. Primary interviews are done with players involved in each phase of a supply chain to analyze the market forecasting. The secondary research method is used to help you fully understand how the future markets and the spending patterns look likes.

The report is based on in-depth qualitative and quantitative analysis of the Product Market. The quantitative analysis involves the application of various projection and sampling techniques. The qualitative analysis involves primary interviews, surveys, and vendor briefings. The data gathered as a result of these processes are validated through experts opinion. Our research methodology entails an ideal mixture of primary and secondary initiatives.

Frequently Asked Questions About This Report

PLACE AN ORDER

Year End Discount

Sample Report

Pre-Purchase Inquiry

NEED CUSTOMIZATION?

Request CustomizationCALL OR EMAIL US

100% Secure Payment

Related Reports

Have a glance of the Report

Our Global Clients

Our data-driven insights have influenced the strategy of 200+ reputed companies across the globe.