The global dental 3D printing market is expected to grow at a CAGR of 29.5% from 2021 to reach USD 7.8 billion by 2027. The growth is primarily attributed to rising incidence of dental caries & related dental problems, growing demand for cosmetic dentistry, rapidly growing geriatric population and high adoption of dental 3D printing in hospitals and clinics. However, financial constraints in small to medium sized laboratories pose significant challenge to the growth of dental 3D printing market.

By Product: Services segment dominated the dental 3D printing market

Services segment accounted for the largest share of dental 3D printing market. The largest share of this segment is mainly due to competitive pricing offered by dental 3D printing service providers, large scale outsourcing of dental product design and increased production by hospitals, clinics and laboratories.

By Technology: Fused deposition modelling to grow at highest CAGR

On the basis of technology, dental 3D printing market is segmented into VAT photopolymerization, fused deposition modelling, selective laser sintering, PolyJet printing and other technologies. Fused deposition modelling segment accounted for highest CAGR in the forecast period. The growth of this segment is mainly led by low machine & material cost, ability to use several materials simultaneously and availability of wide range of thermoplastics.

By Application, Prosthodontics accounted for the largest market share

Dental 3D printing market is segmented into prosthodontics, implantology and orthodontics on the basis of application. Prosthodontics accounted for highest market share in the dental 3D printing market. The largest market of this segment can be attributed to rising prevalence of dental caries, increasing demand for advanced dental technologies and growing demand for crowns and bridges.

By End User: Dental laboratories segment growing at highest rate

Based on the end user segregation, dental laboratories segment is projected to account for highest CAGR in dental 3D printing market. The growth of this market segment can be explained by increasing adoption of advanced dental technology and consolidation of dental laboratories.

By Region: APAC is the fastest growing regional market while North America maintains lead

In 2020, North America accounted for the largest share of dental 3D printing market. The largest share of this regional segment is mainly due to growing incidence of dental caries and tooth loss, increasing demand for cosmetic dentistry and increasing geriatric population. APAC showed spike in growth due to low cost of operation in these countries and foreign investment policies.

Competitive Scenario

- Stratasys Ltd. (US)

- 3D Systems Inc. (US)

- EnvisionTEC (Germany)

- DWS Systems SRL (Italy)

- Renishaw (UK)

- Formlabs (US)

- Prodways Group (France)

- SLM Solutions Group AG (Germany)

- Carbon Inc. (US)

- Concept Laser (Germany)

- EOS GmbH Electro Optical Systems (Germany)

- Rapid Shape (Germany)

- Asiga (Australia)

- Roland DG (Japan)

- DENTSPLY Sirona Inc. (US)

- SprintRay (US)

- Zortrax (Poland)

- Detax GmbH (Germany)

- DMG America (US)

- 3Dresyns (Spain)

- VOCO GmbH (Germany)

- Dental Solutions Israel (Israel)

- TRUMPF (Germany)

- 3BFab (Turkey)

- and Keystone Industries (US).

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.2.4. Challenges

4.3. COVID-19 Impact of the dental 3D printing market

5. Industry Insights

5.1. Introduction

5.2. Industry Trends

6. Global Dental 3D Printing Market, By Product, 2019-2027 (USD Million)

6.1. Introduction

6.2. Services

6.3. Materials

6.4. Equipment

7. Global Dental 3D Printing Market, By Technology, 2019-2027 (USD Million)

7.1. VAT Photopolymerization

7.2. Fused deposition modelling

7.3. Selective laser sintering

7.4. PolyJet printing

8. Global Dental 3D Printing Market, By Application, 2019-2027 (USD Million)

8.1. Prosthodontics

8.2. Orthodontics

8.3. Implantology

9. Global Dental 3D Printing Market, By End User, 2019-2027 (USD Million)

9.1. Dental laboratories

9.2. Dental hospitals & clinics

9.3. Dental academic & research institutes

10. Global Dental 3D Printing Market, By Geography, 2019-2027 (USD Million)

10.1. North America

10.1.1. US

10.1.2. Canada

10.2. Europe

10.2.1. Germany

10.2.2. UK

10.2.3. France

10.2.4. Italy

10.2.5. Spain

10.2.6. Rest of Europe

10.3. Asia-Pacific

10.3.1. China

10.3.2. Japan

10.3.3. India

10.3.4. Rest of Asia-Pacific

10.4. Rest of the World

10.4.1. Latin America

10.4.2. Middle East & Africa

11. Copetitive Landscape

11.1. Introduction

11.2. Market Share Analysis

11.3. Competitive Situation and Trends

11.3.1. Product Launches

11.3.2. Partnerships, Collaborations and Agreements

11.3.3. Acquisitions

11.3.4. Expansions

11.3.5. Other Developments

12. Company Profiles

12.1. Zoetis, Inc. (US)

12.2. Stratasys Ltd. (US)

12.3. 3D Systems, Inc. (US)

12.4. EnvisionTEC (Germany)

12.5. DWS Systems SRL (Italy)

12.6. Renishaw (UK)

12.7. Formlabs (US)

12.8. Prodways Group (France)

12.9. SLM Solutions Group AG (Germany)

12.10. Carbon, Inc. (US)

12.11. Concept Laser (Germany)o

12.12. EOS GmbH Electro Optical Systems (Germany)

12.13. Rapid Shape (Germany)

12.14. Asiga (Australia)

12.15. Roland DG (Japan)

12.16. DENTSPLY Sirona, Inc. (US)

12.17. SprintRay (US)

12.18. Zortrax (Poland)

12.19. Detax GmbH (Germany)

12.20. DMG America (US)

12.21. 3Dresyns (Spain)

12.22. VOCO GmbH (Germany)

12.23. Dental Solutions Israel (Israel)

12.24. TRUMPF (Germany)

12.25. 3BFab (Turkey)

12.26. Keystone Industries (US)

13. Appendix

13.1. Discussion Guide

13.2. Available Customizations

13.3. Related Reports

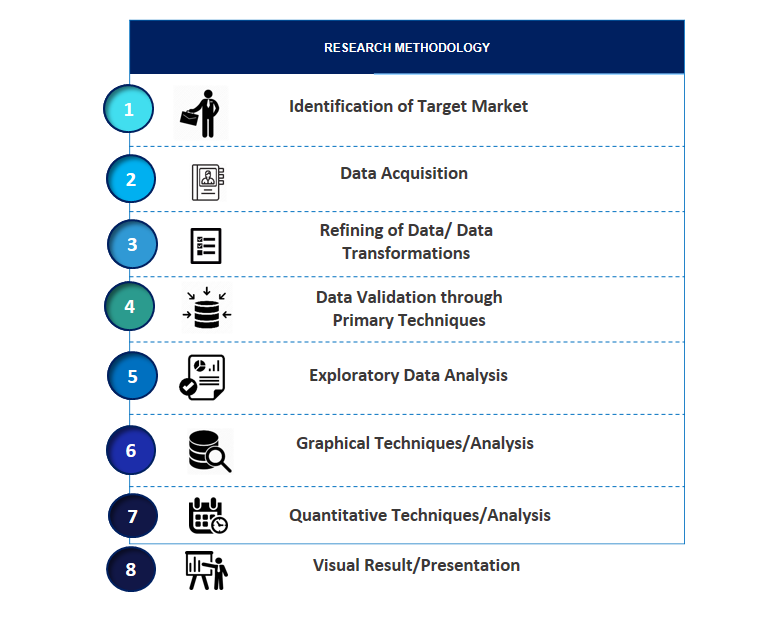

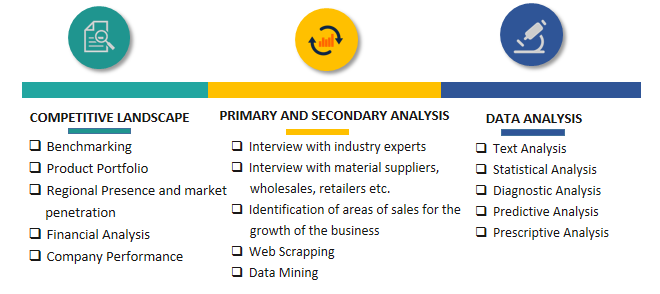

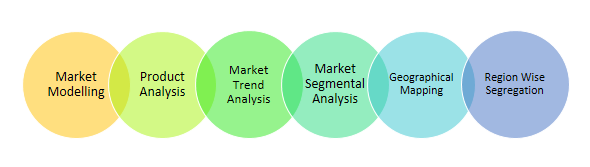

SPER Market Research’s methodology uses great emphasis on primary research to ensure that the market intelligence insights are up to date, reliable and accurate. Primary interviews are done with players involved in each phase of a supply chain to analyze the market forecasting. The secondary research method is used to help you fully understand how the future markets and the spending patterns look likes.

The report is based on in-depth qualitative and quantitative analysis of the Product Market. The quantitative analysis involves the application of various projection and sampling techniques. The qualitative analysis involves primary interviews, surveys, and vendor briefings. The data gathered as a result of these processes are validated through experts opinion. Our research methodology entails an ideal mixture of primary and secondary initiatives.