5G in Healthcare Market Growth, Upcoming Trends and Future Demand 2030

5G in Healthcare Market Size, Share & Trends Analysis By Component, By Application, By End User, Regional Outlook, Competitive Strategies and Segment Forecasts to 2030

| Published: Jan-2022 | Report ID: HLCA2203 | Pages: 1 - 208 | Formats*: |

| Category : Healthcare | |||

| Report Metric | Details |

| Market size available for years | 2019-2030 |

| Base year considered | 2021 |

| Forecast period | 2022-2030 |

| Segments covered | By Component, By Application, By End User |

| Geographies covered | North America, Europe, APAC, Latin America and the Middle East & Africa |

| Companies Covered | Airtel, AT&T, BT Group, China Mobile Limited, Cisco, Deutsche Telekom AG, Ericsson, Fibocom Wireless Inc., Huawei Technologies Co. Ltd., NEC Corporation, Nokia, NTT DOCOMO, Orange S.A. , Qualcomm, Quectel, Samsung, Sequans, Sierra Wireless, SK Telecom Co. Ltd., Swisscom, Telefónica, Telit, Telus, T-Mobile, Verizon, Vodafone |

4.1. Introduction4.2. Market Dynamics

4.2.1. Drivers4.2.2. Restraints4.2.3. Opportunities4.2.4. Challenges

4.3. COVID-19 Impact of the 5G in Healthcare Market4.4. Market Trends

5.1. Hardware5.2. Services5.3. Connectivity

6.1. Connected Medical Devices6.2. Remote Patient Monitoring6.3. AR/VR6.4. Asset tracking for medical devices6.5. Connected Ambulance

7.1. Healthcare Providers7.2. Healthcare Payers7.3. Other End Users

8.1. North America

8.1.1. US8.1.2. Canada

8.2. Europe

8.2.1. Germany8.2.2. UK8.2.3. France8.2.4. Italy8.2.5. Spain8.2.6. Rest of Europe

8.3. Asia-Pacific

8.3.1. China8.3.2. Japan8.3.3. India8.3.4. Rest of Asia-Pacific

8.4. Rest of the World

8.4.1. Latin America

8.4.2. Middle East & Africa

9.1. Introduction9.2. Market Share Analysis, By Key Players9.3. Competitive Scenario

9.3.1. Product Launches9.3.2. Partnerships, Collaborations and Agreements9.3.3. Acquisitions9.3.4. Expansions9.3.5. Other Developments

10.1. Airtel10.2. AT&T10.3. BT Group10.4. China Mobile Limited10.5. Cisco10.6. Deutsche Telekom AG10.7. Ericsson10.8. Fibocom Wireless Inc.10.9. Huawei Technologies Co., Ltd.10.10. NEC Corporation10.11. Nokia10.12. NTT DOCOMO10.13. Orange S.A.10.14. Qualcomm10.15. Quectel10.16. Samsung10.17. Sequans10.18. Sierra Wireless10.19. SK Telecom Co., Ltd.10.20. Swisscom10.21. Telefónica10.22. Telit10.23. Telus10.24. T-Mobile10.25. Verizon10.26. Vodafone

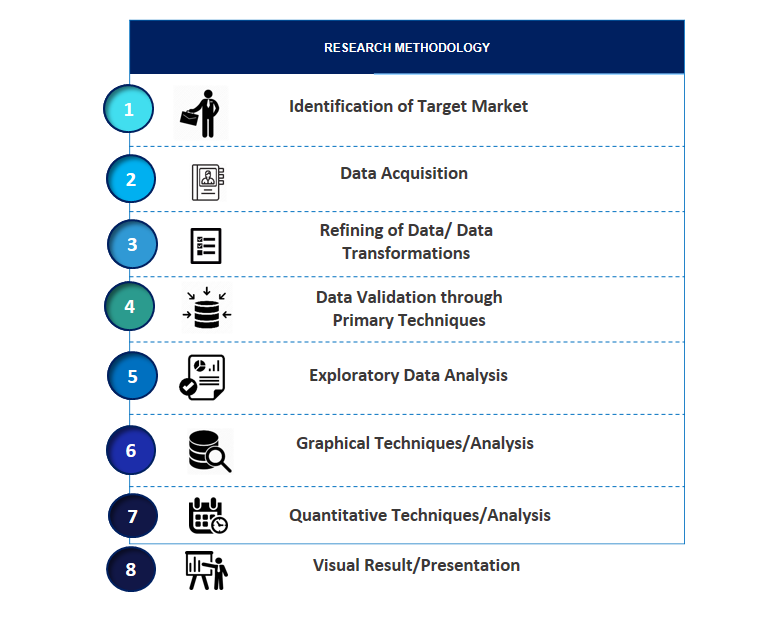

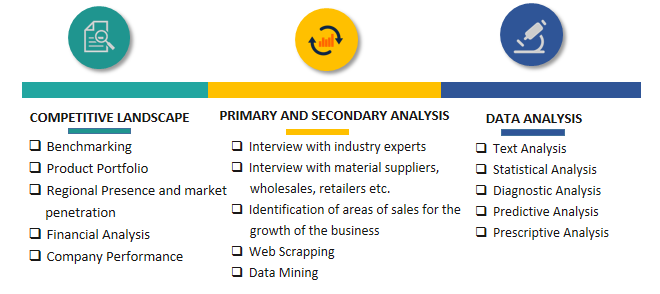

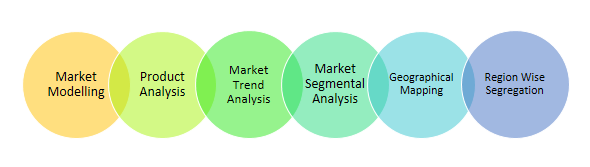

SPER Market Research’s methodology uses great emphasis on primary research to ensure that the market intelligence insights are up to date, reliable and accurate. Primary interviews are done with players involved in each phase of a supply chain to analyze the market forecasting. The secondary research method is used to help you fully understand how the future markets and the spending patterns look likes.

The report is based on in-depth qualitative and quantitative analysis of the Product Market. The quantitative analysis involves the application of various projection and sampling techniques. The qualitative analysis involves primary interviews, surveys, and vendor briefings. The data gathered as a result of these processes are validated through experts opinion. Our research methodology entails an ideal mixture of primary and secondary initiatives.

Frequently Asked Questions About This Report

PLACE AN ORDER

Year End Discount

Sample Report

Pre-Purchase Inquiry

NEED CUSTOMIZATION?

Request CustomizationCALL OR EMAIL US

100% Secure Payment

Related Reports

Have a glance of the Report

Our Global Clients

Our data-driven insights have influenced the strategy of 200+ reputed companies across the globe.